The PRA published its business plan earlier in April and as with the FCA, there is unsurprisingly quite a significant focus on how it will deliver its new growth objectives now these are formally in place. As Sam Woods says in the foreword, it will be the first full year for the PRA operating under the Financial Services and Markets Act 2023, under which the growth objective has been introduced. It is one of two key points he highlights, alongside their ongoing programme of work to maintain the resilience of the financial sector.

The objectives bring with them a significant ‘to do’ list and as is the case with the FCA, the PRA plans to use data and analytics to improve how it works. With the commitment to utilising the freedoms that have been introduced with the Brexit-related changes we are promised simplification of the regulatory regime, with a more pragmatic approach that seeks to make the UK a more attractive place for investment, for UK owned businesses or international firms seeking to expand into the UK market.

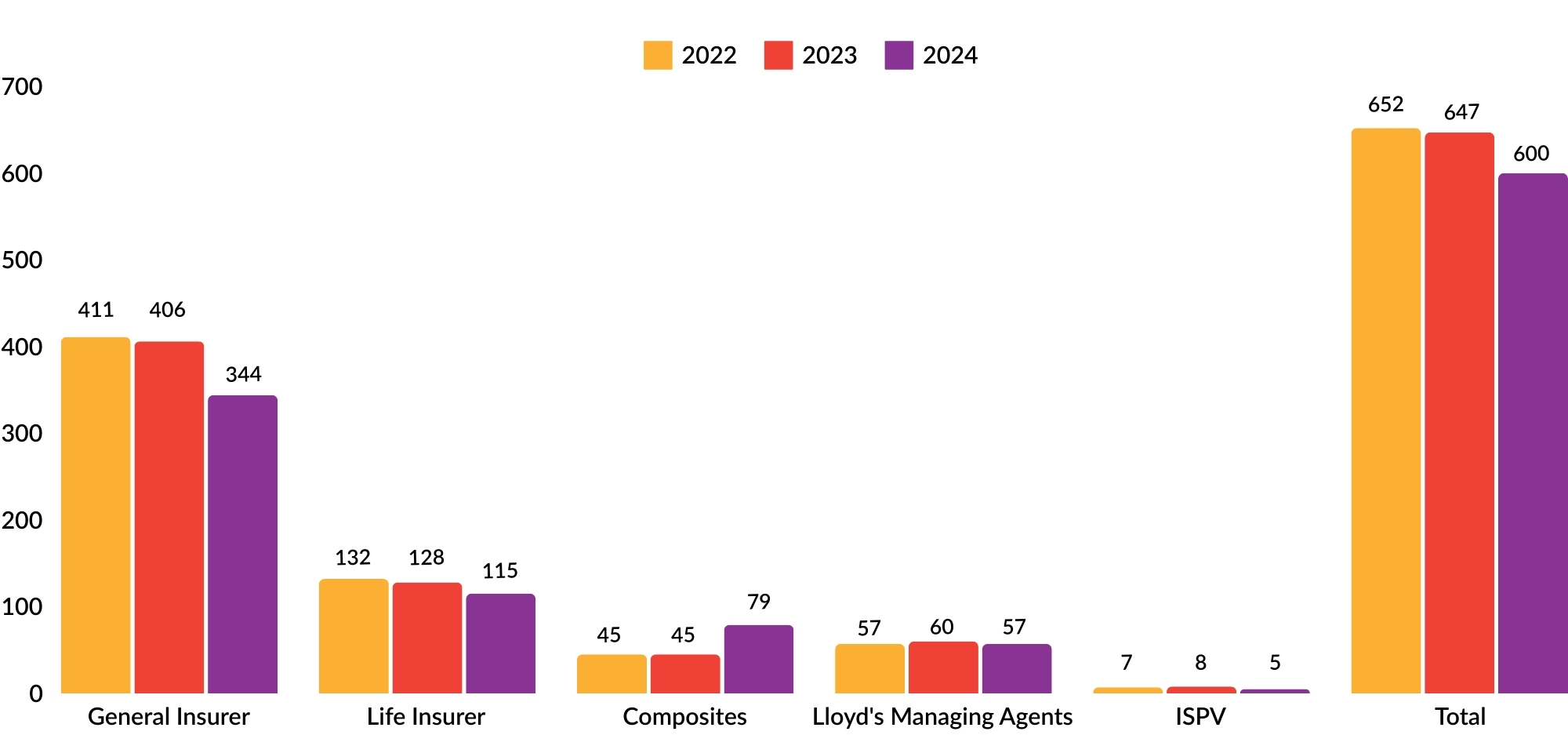

With so much focus on the new secondary objective, it’s interesting to take a look at the data from the last 3 years setting out the number of supervised insurers, by type, as reported by the PRA. In every category, except ‘composites’, the number has reduced, as has the overall number – from 652 firms in 2022 to 600 firms as at January 2024.

Against the background of a Business Plan focused on growth, there is a sense of irony that the number of supervised firms has been in decline for a few years now. Any easing of the regulatory burden for the PRA at a firm level will though be more than offset by initiatives such as the update to the Solvency regime which continues to absorb a significant amount of PRA resource.

Strategic Objectives

The PRA strategic objectives are unchanged from those set out 12 months ago, which were already aligned to the new powers, new secondary objective, and expanded role contemplated by what was then the forthcoming Financial Services and Markets Act 2023. These objectives are to:

- maintain and build on the safety and soundness of the banking and insurance sectors, and ensure continuing resilience,

- be at the forefront of identifying new and emerging risks, and developing international policy,

- support competitive and dynamic markets, alongside facilitating international competitiveness and growth, in the sectors that the PRA regulates, and

- run an inclusive, efficient, and modern regulator within the central bank.

The plan offers clear guidance on how the PRA intends to deliver those objectives, including the politically-driven ‘Brexit’, with much of the PRA focus and resource remaining committed to the way it helps ensure the UK derives the benefits promised from those reforms. The detail of those changes is rapidly becoming clear, and the implementation timelines are now very much on the near-term horizon for firms. Whatever your views on the rights and wrongs of Brexit itself, we will soon have a very clear idea on whether or not the promised benefits for our industry and the UK economy can be delivered by these changes.

The 2024/5 Business Plan – The Detail

There may be little in terms of new policy or activity in the Business Plan, but there is most certainly a lot of detail to digest. We’ve pulled out the key activities, themes and issues that are relevant to insurance firms – as ever, insurance firms often seem to be playing ‘second fiddle’ to our colleagues in the banking sector. If you have any questions about the individual areas, please do speak with a member of the ICSR team.

Safety, Soundness & Resilience

There are two key sections to the way the PRA seeks to deliver this objective. These are:

- Financial Resilience (for Insurers), and

- Regulatory reforms.

Financial resilience – insurers

The focus here is on delivering the benefits of Brexit, with the PRA working towards the conclusion of change necessitated by the repeal and replacement of EU laws and specifically the move from Solvency II to Solvency UK rules. In June 2024 the PRA has said it will publish its final policy on the matching adjustment (MA) reforms and it promises to streamline the application processes for new internal model permissions and variations of existing permissions. It has promised to establish dedicated, specialised teams for reviewing applications, which is to be welcomed, but has caveated this by saying that delivery of timely decisions will be dependent on good engagement between firms and the PRA. If you would like to understand more about what that engagement looks like, do talk to one of the ICSR team.

The PRA has now also published CP5/24 – Review of Solvency II: Restatement of assimilated law which sets out the final PRA rules and other policy materials that will replace Solvency II assimilated law which is being revoked by the Government under its Smart Regulatory Framework. (You can find all of our articles on Solvency here.)

Other areas of focus for the financial resilience of our sector include:

- Insurance stress testing

The next major Life Insurance stress testing takes place in 2025, when the PRA will also run its first dynamic stress test for General Insurers. More details on participation, design, and timelines are promised during 2024. - Cyber underwriting risk

The PRA see the uncertainty of this risk, robust risk management, risk appetite-setting, and stress testing as important factors in ensuring that capital and exposure management capabilities reflect firms’ actual exposures to these risks, with a specific concern flagged around “contract (un)certainty” as it terms the issue – insurance contracts that do not necessarily clearly address the question of policy cover and exclusions for this issue. - Model drift

The PRA has concerns over the robustness of models used across the market. It also seeks to improve the effectiveness of internal model validation, to help firms develop the capability to self-identify and address potential challenges. - Funded reinsurance

The PRA has concerns about the rapidly increasing use of funded reinsurance transactions in the life insurance market, and the risks this may pose to policyholder protection and financial stability. It flagged those concerns in its 11th January Insurance Supervision Priorities and reminds firms that it did so. - Impact on general and claims inflation

The PRA sees claims inflation as a ‘significant risk’ for general insurers and expects a continued lag in the emergence of claims inflation. It is monitoring carefully through regulatory data and warns of the possibility of further action. - Liquidity risk management

The PRA remains concerned about gaps in insurers’ liquidity risk management frameworks and new liquidity reporting requirements for those insurance firms most exposed to liquidity risk are planned. - Credit risk management

The PRA will continue to focus on the effectiveness of firms’ credit risk management capabilities and seek further assurance that firms’ internal credit assessments appropriately reflect the risk profile of their asset holdings.

Regulatory Reform

None of the areas of regulatory reform are new, but they most certainly reflect areas where there is still work to be done or reform remains necessary.

- Operational risk and resilience and Critical Third Parties

An area where the Bank of England, PRA and FCA have jointly acted, the original rules came into effect in March 2022, with firms expected to have delivered on their plans to deliver important business services within defined impact tolerances during severe but plausible scenarios by no later than March 2025. The PRA will be assessing progress on this. It is also developing regulatory expectations on incident reporting. A further consultation paper relating to CTPs is expected later this year. (You can find all of our articles and webinars on the subject of Operational Resilience here.) - Review of enforcement policies

The PRA published a new approach to enforcement in January 2024: PS1/24 – The Bank of England’s approach to enforcement. This introduced a new mechanism for early cooperation and greater incentives for early admissions of failings by firms. If you would like any guidance on how this approach works, please do speak with any of the directors of ICSR in complete confidence. - Diversity and inclusion in PRA-regulated firms

The PRA sees a clear link between diversity & inclusivity and the ability of firms to support better governance, decision-making, and risk management, reduce groupthink and promote a culture that allows employees to feel able to speak up and challenge the status quo. This work has been a long-time coming and all we are promised in 2024 is ‘a further update in due course’.

Emerging Risks and International Policy

The PRA sees for itself a significant role on the international stage, helping identify risk and shape international response. It is consistent with the Government objective to put the UK financial markets at the centre of international systems and position our banking and insurance sectors as international leaders. It is certainly a path to driving growth. The key elements that will affect the UK insurance market include:

- Third Country Branches

The way the PRA seek to promote international collaboration, setting out clear expectations for firms wanting to branch into the UK. - Operational and cyber resilience

The PRA engages internationally on operational and cyber resilience, in support of its supervision objectives and to raise international standards. This work will be closely linked to the firm related work already highlighted earlier in this article. - Climate Change

The risks arising from climate change are seen by the PRA as a source of material and increasing financial risk to firms and the financial system. In its Supervisory Priorities letter dated 11th January 2024, the PRA set out its expectations of firms and it uses the Business Plan as an opportunity to issue a reminder. It plans to update it’s last major Supervisory Statement, dating from 2019, on the subject later this year. We talked about the issue of Climate Risk back in January in this article: Climate Change Disclosure – Managing Multiple Stakeholders. - Artificial Intelligence and Machine Learning

The PRA and FCA intend to jointly conduct the third edition of a joint survey on machine learning in UK financial services Q2 2024. No specific timing is given for the next steps, but we can expect an update on the issues and risks posed by AI/ML later in 2024 or early 2025.

Competitive and dynamic markets

We often hear the Regulators talk about proportionality and here, we see the PRA give a further commitment to this when they say:

“The PRA will go further in developing proportionate and efficient prudential requirements, thereby reducing the burden on firms where appropriate, and pursuing its secondary objectives.”

Much of this will be delivered under the Smarter Regulatory Framework banner, with the detail really coming with the completion of the repeal and replacement of Solvency II files expected by the end of 2024.

- Secondary competitiveness and growth objective (SCGO)

The PRA has committed to launching a research programme to deepen its understanding of the ways prudential requirements affect the international competitiveness and growth of the UK economy. The approach focuses on strengthening the three regulatory foundations that were set out in CP27/23:- Maintaining trust among domestic and foreign firms in the PRA and UK prudential framework;

- Adopting effective regulatory processes and engagement

- Taking a responsive and responsibly open approach to UK risks and opportunities

- Insurance Special Purpose Vehicles regime

This regime has been less successful than the PRA expected – we saw how few firms are actually supervised under this at the beginning of this article. The PRA remains committed to the idea and expects to consult on some changes. - Remuneration reforms

The PRA is considering the need for further change to help advance its objectives. - Senior Managers & Certification Regime (SM&CR)

HM Treasury launched a call for evidence alongside the work launched by the PRA and FCA. It would appear HMT have now almost completed their exercise of reviewing the feedback given – which had to be submitted by 1st June 2023 – and the PRA intends to consult on further changes in H1 2024. (You can find all of our articles on SM&CR here and our recent Podcast episode talking about SM&CR) - PRA Rulebook

We are promised a simpler rulebook split into three areas:- Rules,

- supervisory statements, and

- statements of policy.

Many will welcome this after finding navigating the PRA website somewhat complex.

- Supporting and authorising new market entrants via new ‘mobilisation’ regime

The PRA have committed to mirroring the approach adopted for banking, with a new ‘mobilisation’ regime to facilitate entry and expansion for new insurers from 31 December 2024. The intent is to facilitate competition, international competitiveness and growth in the UK insurance sector. If you are thinking of entering the UK market and want to know more about what this might mean for your plans, do speak with any of the directors. - Ease of exit

A further Policy Statement on solvent exit planning for insurers is expected in H2 2024, following the completion of the market consultation initiated by CP2/24 – Solvent exit planning for insurers.

Running an inclusive, efficient, and modern regulator

In his foreword, Sam Woods talked about the increasing importance of data and this is alluded to again as it commits to a programme of work to strengthen and transform its data-related capabilities. The recent Memorandum of Understanding signed with the FCA will help it on that front. It has also set out an agenda for its research priorities, all of which are designed to help the PRA deliver on its objectives more efficiently.

But having talked about the drive for operational efficiency and the maintenance of its headcount at around the same level, the PRA has set a budget that shows an 11% increase over last year – trumping the FCA increase of 10.7%.

Conclusion

The PRA Business Plan for 2024/5 reflects the strong influence of our current government’s priorities – to deliver and demonstrate the opportunities that arise from our decision to exit from the EU and forge our own path internationally. There are significant growth-related elements to the plan that seek to capitalise on our ability to set our own agenda and encourage investment and growth within the UK. London has always enjoyed the status of an international leader for the provision of insurance and there is certainly a strong expectation that the PRA actions will help deliver growth through the facilitation of new investments.

The decline in numbers of supervised firms over the last few years is explained in a number of ways, including ongoing consolidation in the market, the withdrawal of some non-UK firms who have chosen to exit the UK market following Brexit rather than seek authorisation under the new regime, and in a few instances, failure of firms. But with that reduction in number of firms, and the ongoing general attraction of London as an international insurance market, it is easy to see why new firms might be attracted to set up in the UK. Their options for doing so are increasing, and the regulatory environment under which they would be required to operate, including that imposed by our Regulator of conduct, the FCA, are, in our view, becoming more attractive. That combination should prove an effective catalyst for investment and growth.

If you have any questions about the PRA Business Plan for 2024/5, or the issues discussed in this article, please speak with either of the authors or your usual ICSR contact.

Useful Links

The PRA Business Plan references a number of other key documents. Links to these are provided below for ease.

Kenneth Underhill

Director